UNITED

STATES

SECURITIES AND

EXCHANGE COMMISSION

Washington, D.C.

20549

FORM

10-Q

(Mark

One)

☒

Quarterly Report Pursuant to

Section 13 or 15(d) of the Securities Exchange Act of

1934

For the Quarterly

Period Ended March 31, 2021

☐

Transition Report Pursuant to

Section 13 or 15(d) of the Securities Exchange Act of

1934

For the

transition period from

to

Commission File

Number: 001-39070

MONOPAR

THERAPEUTICS INC.

(Exact name of

registrant as specified in its charter)

|

DELAWARE

|

|

32-0463781

|

|

(State or other

jurisdiction of

incorporation or

organization)

|

|

(I.R.S.

employer

identification

number)

|

|

1000 Skokie

Blvd., Suite 350, Wilmette, IL

|

|

60091

|

|

(Address of

principal executive offices)

|

|

(zip

code)

|

(847) 388-0349

(Registrant’s

telephone number, including area code)

Securities

registered pursuant to Section 12(b) of the Act:

|

Title of each

class

|

|

Trading

Symbol(s)

|

|

Name of each

exchange on which registered

|

|

Common Stock,

$0.001 par value

|

|

MNPR

|

|

The Nasdaq Stock

Market LLC

(Nasdaq Capital

Market)

|

Securities

registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark whether the

registrant (1) has filed all reports required to be filed by

Section 13 or 15(d) of the Securities Exchange Act of 1934 during

the preceding 12 months (or for such shorter period that the

registrant was required to file such reports), and (2) has been

subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the

registrant has submitted electronically every Interactive Data File

required to be submitted pursuant to Rule 405 of Regulation S-T

(§ 232.405 of this chapter) during the preceding 12 months (or

for such shorter period that the registrant was required to submit

such files). Yes ☒

No ☐

Indicate by check mark whether the

registrant is a large accelerated filer, an accelerated filer, a

non-accelerated filer, a smaller reporting company, or an emerging

growth company. See the definitions of “large accelerated

filer,” “accelerated filer,” “smaller

reporting company” and “emerging growth company”

in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

☐

|

|

Accelerated filer

|

☐

|

|

Non-accelerated filer

|

☒

|

|

Smaller reporting

company

|

☒

|

|

|

|

|

Emerging growth company

|

☒

|

If an emerging growth company,

indicate by check mark if the registrant has elected not to use the

extended transition period for complying with any new or revised

financial accounting standards provided pursuant to Section 13(a)

of the Exchange Act. ☒

Indicate by check mark whether the

registrant is a shell company (as defined in Rule 12b-2 of the

Act). Yes ☐

No ☒

The number of shares outstanding

with respect to each of the classes of our common stock, as of

April 30, 2021, is set forth below:

|

Class

|

|

Number of shares

outstanding

|

|

|

Common Stock, par value $0.001 per

share

|

|

12,569,933

|

|

|

|

|

|

|

MONOPAR

THERAPEUTICS INC.

TABLE OF

CONTENTS

|

Part I

|

|

|

|

FINANCIAL INFORMATION

|

|

Page

|

|

|

|

|

|

|

|

|

|

|

|

Item 1.

|

|

|

|

3

|

|

|

|

|

|

|

|

3

|

|

|

|

|

|

|

|

4

|

|

|

|

|

|

|

|

5

|

|

|

|

|

|

|

|

7

|

|

|

|

|

|

|

|

8

|

|

|

|

Item 2.

|

|

|

|

20

|

|

|

|

Item 4.

|

|

|

|

33

|

|

|

|

|

|

|

|

|

|

Part II

|

|

|

|

OTHER INFORMATION

|

|

|

|

|

|

Item 1A.

|

|

|

|

34

|

|

|

|

Item 6.

|

|

|

|

35

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

36

|

|

|

|

|

|

|

|

|

Forward-Looking

Statements

This Quarterly Report on Form 10-Q

contains “forward-looking statements” within the

meaning of Section 27A of the Securities Act of 1933, as amended

(the “Act”) and Section 21E of the Securities Exchange

Act of 1934, as amended. All statements other than statements of

historical facts included in this Quarterly Report on Form 10-Q are

forward-looking statements. The words “hopes,”

“believes,” “anticipates,”

“plans,” “seeks,” “estimates,”

“projects,” “expects,”

“intends,” “may,” “could,”

“should,” “would,” “will,”

“continue,” and similar expressions are intended to

identify forward-looking statements. The following uncertainties

and factors, among others, could affect future performance and

cause actual results to differ materially from those matters

expressed in or implied by forward-looking statements:

●

our ability to

raise sufficient funds in the next 12 months in order for us to

complete the Phase 3 portion of our Validive Phase 2b/3 clinical

trial and if required complete a smaller second confirmatory Phase

3 clinical trial, to continue the clinical development of

camsirubicin beyond the dose escalation run-in clinical trial, to

support further development of potential radio-immuno-therapeutics

to treat severe COVID-19 (patients with SARS-CoV-2 infection), to

support further development of MNPR-101 and related compounds and

generally to support our current and any future product candidates

through completion of clinical trials, approval processes and, if

applicable, commercialization;

●

our ability to find a suitable pharmaceutical

partner to further our development efforts, if we are unable to

raise sufficient additional financing;

●

risks and uncertainties associated with our

research and development activities, including our clinical

trials;

●

estimated timeframes for our clinical trials and

regulatory reviews for approval to market products;

●

plans to research, develop, gain approval and

commercialize our current and future product

candidates;

●

the rate of market acceptance and the

competitive clinical efficacy and safety of any products for which

we receive marketing approval;

●

the difficulties of commercialization, marketing

and product manufacturing and overall strategy;

●

uncertainties of intellectual property position

and strategy;

●

delivering strong future financial

performance;

●

our ability to attract and retain key

personnel;

●

the risks inherent in our estimates regarding

expenses, capital requirements and the availability of additional

financing;

●

the impact of government laws and regulations

including increased governmental control of

healthcare;

●

the uncertain impact of the COVID-19 pandemic on

our ability to advance our clinical programs and raise additional

financing; and

●

uncertainty of financial and operational

projections.

Although we believe that the

expectations reflected in such forward-looking statements are

appropriate, we can give no assurance that such expectations will

be realized. Cautionary statements are disclosed in this Quarterly

Report on Form 10-Q. All subsequent written and oral

forward-looking statements attributable to us or persons acting on

our behalf are expressly qualified in their entirety by the

cautionary statements. We undertake no obligation to update any

statements made in this Quarterly Report on Form 10-Q or elsewhere,

including without limitation any forward-looking statements, except

as required by law.

Any forward-looking statements in this

Quarterly Report on Form 10-Q reflect our current views with

respect to future events or to our future financial performance and

involve known and unknown risks, uncertainties and other factors

that may cause our actual results, performance or achievements to

be materially different from any future results, performance or

achievements expressed or implied by these forward-looking statements.

Information that is based on estimates, forecasts, projections,

market research or similar methodologies is inherently subject to

uncertainties and actual events or circumstances may differ

materially from events and circumstances reflected in this

information.

Risks Associated

With Our Business

Our business is

subject to numerous risks and uncertainties, including those

highlighted in “Item 1A - Risk Factors” of our Annual

Report on Form 10-K filed with the Securities and Exchange

Commission on March 25, 2021. These risks include, among others,

the following:

●

We are a clinical stage

biopharmaceutical company with a history of financial losses. We

expect to continue to incur significant losses for the foreseeable

future and may never achieve or maintain cash self-sufficiency or

profitability, which could result in a decline in the market value

of our common stock.

●

Funds raised to-date are

not sufficient to 1) complete our Validive Phase 2b/3 ("VOICE")

clinical program, including, if required, completing a smaller

second Phase 3 confirmatory clinical trial; 2) continue the

clinical development of camsirubicin beyond the dose escalation

run-in clinical trial; or 3) to support continued development of

MNPR-101 and related compounds. If we are unable to raise enough

funds in the next 12 months from the sale of our common stock or

other financing efforts, we will have to consider strategic options

such as out-licensing Validive or other product candidates,

entering into a clinical or commercial partnership, or terminating

one or more programs. There can be no assurance that we can find a

suitable partner on satisfactory terms.

●

We have a limited operating

history, no revenues from operations, and are dependent upon

raising capital to continue our drug development

programs.

●

We do not have and may

never have any approved products on the market. Our business is

highly dependent upon receiving approvals from various U.S. and

international governmental agencies and will be severely harmed if

we are not granted approval to manufacture and sell our product

candidates.

●

Our clinical trials may not

yield sufficiently conclusive results for regulatory agencies to

approve the use of our products, which will adversely affect our

financial condition.

●

If we experience delays or

difficulties in the enrollment of subjects in clinical trials, our

receipt of necessary regulatory approvals will be delayed or

prevented, which will materially delay our program schedules and

adversely affect our financial condition.

●

We rely on third parties to

conduct our drug product manufacturing, non-clinical studies, and

our clinical trials. If these third parties do not or cannot

successfully carry out their contractual duties or meet expected

deadlines or performance goals, the initiation or conduct of our

clinical trials may be delayed and we may be unable to obtain

regulatory approval for, or commercialize, our current product

candidates or any future products, and our financial condition will

be adversely affected.

●

We face significant

competition from other biotechnology and pharmaceutical companies,

in targeted medical indications, and our operating results will

suffer if we fail to compete effectively. Competition and

technological change may make our product candidates obsolete or

non-competitive.

●

The termination of

third-party licenses will adversely affect our rights to important

compounds or technologies.

●

If we and our third-party

licensors do not obtain and preserve protection for our respective

intellectual property rights, our competitors may be able to

develop competing drugs, which will adversely affect our financial

condition.

●

If we lose key management

leadership, and/or scientific personnel, and if we cannot recruit

qualified employees or other significant personnel for future

personnel requirements, we may experience program delays and

increased compensation and operational costs, and our business will

be materially disrupted.

●

The COVID-19 pandemic could

have a substantial negative impact on our business, financial

condition, operating results, stock price and ability raise

additional funds.

PART

I

Item 1. Financial

Statements

Monopar

Therapeutics Inc.

Condensed

Consolidated

Balance

Sheets

(Unaudited)

|

|

|

|

|

Assets

|

|

|

|

Current

assets:

|

|

|

|

Cash and cash

equivalents

|

$25,723,113

|

$16,737,109

|

|

Other current

assets

|

114,569

|

62,690

|

|

Total current

assets

|

25,837,682

|

16,799,799

|

|

|

|

|

|

Other non-current

assets

|

68,858

|

68,858

|

|

Total

assets

|

$25,906,540

|

$16,868,657

|

|

Liabilities and Stockholders'

Equity

|

|

|

|

Current

liabilities:

|

|

|

|

Accounts payable,

accrued expenses and other current liabilities

|

$806,272

|

$1,176,666

|

|

Total current

liabilities and total liabilities

|

806,272

|

1,176,666

|

|

|

|

|

|

Commitments and

contingencies (Note 6)

|

|

|

|

Stockholders’

equity:

|

|

|

|

Common stock, par value

of $0.001 per share, 40,000,000 shares authorized, 12,569,933 and

11,453,465 shares issued and outstanding at March 31, 2021 and

December 31, 2020, respectively

|

12,570

|

11,453

|

|

Additional paid-in

capital

|

59,161,975

|

47,873,570

|

|

Accumulated other

comprehensive loss

|

(5,099)

|

(7,873)

|

|

Accumulated

deficit

|

(34,069,178)

|

(32,185,159)

|

|

Total stockholders'

equity

|

25,100,268

|

15,691,991

|

|

Total liabilities and

stockholders' equity

|

$25,906,540

|

$16,868,657

|

* Derived from the Company’s

audited consolidated financial statements.

The accompanying notes are an

integral

part of these condensed consolidated

financial statements.

Monopar

Therapeutics Inc.

Statements of

Operations and Comprehensive Loss

(Unaudited)

|

|

For the Three Months Ended

March 31,

|

|

|

|

|

|

Operating

expenses:

|

|

|

|

Research and

development

|

$1,206,779

|

$344,407

|

|

General and

administrative

|

687,936

|

791,607

|

|

Total operating

expenses

|

1,894,715

|

1,136,014

|

|

Loss from

operations

|

(1,894,715)

|

(1,136,014)

|

|

Other

income:

|

|

|

|

Interest

income

|

10,696

|

45,137

|

|

Net

loss

|

(1,884,019)

|

(1,090,877)

|

|

Other comprehensive

income (loss):

|

|

|

|

Foreign currency

translation gain (loss)

|

2,774

|

(4,041)

|

|

Comprehensive

loss

|

$(1,881,245)

|

$(1,094,918)

|

|

Net loss per

share:

|

|

|

|

Basic and

diluted

|

$(0.16)

|

$(0.10)

|

|

Weighted average shares

outstanding:

|

|

|

|

Basic and

diluted

|

12,139,422

|

10,608,199

|

The accompanying notes are an

integral

part of these condensed consolidated

financial statements.

Monopar Therapeutics Inc.

Condensed

Consolidated Statements of Stockholders’ Equity

Three Months

Ended March 31, 2020

(Unaudited)

|

|

|

|

|

|

|

|

|

|

|

Additional Paid-in Capital

|

Accumulated Other

Comprehensive Loss

|

|

Total Stockholders'

Equity

|

|

Balance at January 1,

2020

|

10,587,632

|

$10,587

|

$38,508,825

|

$(10,970)

|

$(25,880,586)

|

$12,627,856

|

|

Issuance of common stock under a Capital on

DemandTM

Sales Agreement with JonesTrading Institutional Services LLC, net

in commissions and fees of $16,284

|

33,903

|

34

|

526,109

|

—

|

—

|

526,143

|

|

Issuance of common stock to non-employee

directors pursuant to vested restricted stock units

|

1,288

|

1

|

(1)

|

—

|

—

|

—

|

|

Stock-based compensation (non-cash)

|

—

|

—

|

338,497

|

—

|

—

|

338,497

|

|

Offering costs

|

—

|

—

|

(2,161)

|

—

|

|

(2,161)

|

|

Net loss

|

—

|

—

|

—

|

—

|

(1,090,877)

|

(1,090,877)

|

|

Accumulated other comprehensive

loss

|

—

|

—

|

—

|

(4,041)

|

—

|

(4,041)

|

|

Balance at March 31,

2020

|

10,622,823

|

$10,622

|

$39,371,269

|

$(15,011)

|

$(26,971,463)

|

$12,395,417

|

The accompanying notes are an

integral part of these condensed consolidated financial

statements.

Monopar

Therapeutics Inc.

Condensed

Consolidated Statements of Stockholders’ Equity

Three Months

Ended March 31, 2021

(Unaudited)

|

|

|

|

|

|

|

|

|

|

|

Additional Paid-in Capital

|

Accumulated Other

Comprehensive Loss

|

|

Total Stockholders'

Equity

|

|

Balance at January 1,

2021

|

11,453,465

|

$11,453

|

$47,873,570

|

$(7,873)

|

$(32,185,159)

|

$15,691,991

|

|

Issuance of common stock under a Capital on

DemandTM

Sales Agreement with JonesTrading Institutional Services LLC, net

of commissions and fees of $338,153

|

1,104,047

|

1,104

|

10,924,208

|

—

|

—

|

10,925,312

|

|

Issuance of common stock to non-employee

directors pursuant to vested restricted stock units

|

3,004

|

3

|

(3)

|

—

|

—

|

—

|

|

Issuance of common stock to employees pursuant

to vested restricted stock units, net of taxes

|

6,504

|

7

|

(21,507)

|

—

|

—

|

(21,500)

|

|

Issuance of common stock upon exercise of stock

options

|

2,913

|

3

|

17,475

|

—

|

—

|

17,478

|

|

Stock-based compensation (non-cash)

|

—

|

—

|

368,232

|

—

|

—

|

368,232

|

|

Net loss

|

—

|

—

|

—

|

—

|

(1,884,019)

|

(1,884,019)

|

|

Accumulated other comprehensive

income

|

—

|

—

|

—

|

2,774

|

—

|

2,774

|

|

Balance at March 31,

2021

|

12,569,933

|

$12,570

|

$59,161,975

|

$(5,099)

|

$(34,069,178)

|

$25,100,268

|

The accompanying notes are an

integral part of these condensed consolidated financial

statements.

Monopar

Therapeutics Inc.

Statements of

Cash Flows

(Unaudited)

|

|

For the Three Months Ended

March 31,

|

|

|

|

|

|

Cash

flows from operating activities:

|

|

|

|

Net loss

|

$(1,884,019)

|

$(1,090,877)

|

|

Adjustments to reconcile

net loss to net cash used in operating activities:

|

|

|

|

Stock-based compensation

expense (non-cash)

|

368,232

|

338,497

|

|

Changes in operating assets

and liabilities, net

|

|

|

|

Other current

assets

|

(51,879)

|

(42,084)

|

|

Accounts payable,

accrued expenses and other current liabilities

|

(370,394)

|

(331,106)

|

|

Net cash used in

operating activities

|

(1,938,060)

|

(1,125,570)

|

|

Cash

flows from financing activities:

|

|

|

|

Cash proceeds from the

sales of common stock under a Capital on DemandTM Sales Agreement

with JonesTrading Institutional Services LLC, net of commissions,

fees and offering costs of $338,153 and $34,384 for the three

months ended March 31, 2021 and March 31, 2020,

respectively

|

10,925,312

|

508,044

|

|

Taxes paid related to

net share settlement of vested restricted stock units

|

(21,500)

|

—

|

|

Cash proceeds from the

issuance of stock upon exercise of stock options

|

17,478

|

—

|

|

Net cash provided by

financing activities

|

10,921,290

|

508,044

|

|

Effect of exchange

rates

|

2,774

|

(4,041)

|

|

Net increase (decrease)

in cash and cash equivalents

|

8,986,004

|

(621,567)

|

|

Cash

and cash equivalents at beginning of period

|

16,737,109

|

13,213,929

|

|

Cash

and cash equivalents at end of period

|

$25,723,113

|

$12,592,362

|

The accompanying notes are an

integral

part of these condensed consolidated

financial statements.

MONOPAR

THERAPEUTICS INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

March 31,

2021

Note

1 - Nature of Business and Liquidity

Nature of

Business

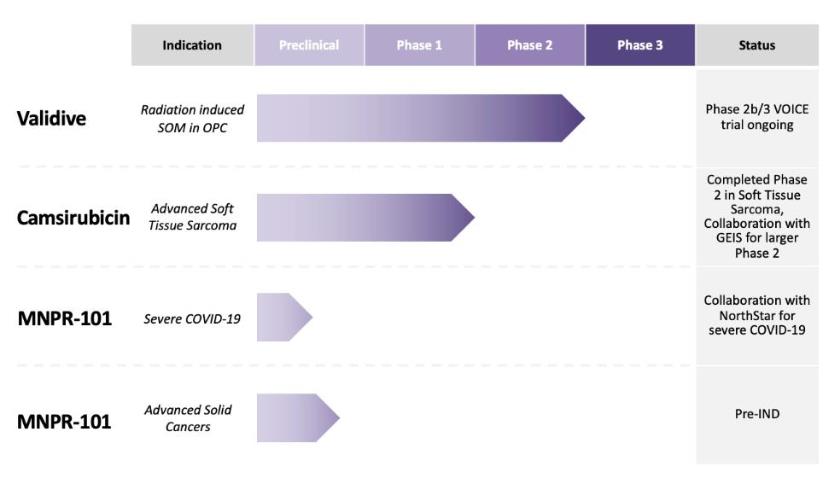

Monopar Therapeutics Inc.

(“Monopar” or the “Company”) is a

clinical-stage biopharmaceutical company primarily focused on

developing proprietary therapeutics designed to extend life or

improve quality of life for cancer patients. Monopar currently has

three compounds in development: 1) Validive® (clonidine

mucobuccal tablet; clonidine MBT), a Phase 2b/3 clinical stage,

first-in-class mucoadhesive buccal tablet for the prevention of

radiation induced severe oral mucositis (“SOM”) in

oropharyngeal cancer patients; 2) camsirubicin (generic name for

MNPR-201, GPX-150; 5-imino-13-deoxydoxorubicin), a clinical stage

topoisomerase II-alpha selective novel analog of doxorubicin

engineered specifically to retain anticancer activity while

minimizing toxic effects on the heart; and 3) a preclinical stage

uPAR targeted antibody, MNPR-101 and related compounds, for

advanced cancers and severe COVID-19.

Liquidity

The Company has incurred an

accumulated deficit of approximately $34.1 million as of March 31,

2021. To date, the Company has primarily funded its operations with

the net proceeds from the Company’s initial public offering

of its common stock on Nasdaq, sales of its common stock in the

public market under a Capital on DemandTM Sales Agreement,

private placements of convertible preferred stock and of common

stock and cash provided in the camsirubicin asset purchase

transaction. Management estimates that currently available cash

will provide sufficient funds to enable the Company to meet its

planned obligations at least through June 2022. The Company’s

ability to fund its future operations, including the clinical

development of Validive and camsirubicin, is dependent upon its

ability to execute its business strategy, to obtain additional

funding and/or to execute collaborative research agreements. There

can be no certainty that future financing or collaborative research

agreements will occur at a time needed to maintain operations, if

at all.

In December 2019, a novel strain of

coronavirus (“COVID-19”) surfaced in China and spread

to essentially all of the remaining world. By March 2020 COVID-19

was designated a global pandemic, resulting in government-mandated

travel restrictions and temporary shutdowns or limitations of

non-essential businesses in many states in the U.S. The Company is

able to remain open but has allowed its employees to work from

home, if required by local authorities. In response to the current

COVID-19 pandemic and its effects on clinical trials, Monopar has

modified the original adaptive design Phase 3 clinical trial for

its lead product candidate, Validive, to be a Phase 2b/3 clinical

trial (“VOICE”) to better fit the types of trials which

can enroll patients in the current environment. This modification

allowed the Company to activate the VOICE clinical trial without

requiring near-term financing. To complete the VOICE clinical

program, including, if required, completing a smaller second Phase

3 confirmatory clinical trial, Monopar will require additional

funding in the millions or tens of millions of dollars (depending

on if the Company has consummated a collaboration or partnership or

neither for Validive), which it is planning to pursue in the next

12 months. Due to many uncertainties, the Company is unable to

estimate the pandemic’s financial impact or duration at this

time, or its potential impact on the Company’s current

clinical trials including the pandemic’s effect on drug

candidate manufacturing, shipping, patient recruitment at clinical

sites and regulatory agencies around the globe.

Note 2 -

Significant Accounting Policies

Basis of

Presentation

These condensed consolidated

financial statements include the financial results of Monopar

Therapeutics Inc., its wholly-owned French subsidiary, Monopar

Therapeutics, SARL, and its wholly-owned Australian subsidiary,

Monopar Therapeutics Australia Pty Ltd and have been prepared in

accordance with accounting principles generally accepted in the

U.S. (“GAAP”) and include all disclosures required by

GAAP for financial reporting. All intercompany accounts have been

eliminated. The principal accounting policies applied in the

preparation of these condensed consolidated financial statements

are set out below and have been consistently applied in all periods

presented. The Company has been primarily involved in performing

research activities, developing product candidates, and raising

capital to support and expand these activities.

MONOPAR

THERAPEUTICS INC.

NOTES TO

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31,

2021

The accompanying unaudited condensed

consolidated financial statements contain all normal, recurring

adjustments necessary to present fairly the Company’s

condensed consolidated financial position as of March 31, 2021, and

the Company’s condensed consolidated results of operations

and comprehensive loss and the Company’s condensed

consolidated cash flows for the three months ended March 31, 2021

and 2020.

The condensed consolidated results

of operations and comprehensive loss and condensed consolidated

cash flows for the periods presented are not necessarily indicative

of the consolidated results of operations or cash flows which may

be reported for the remainder of 2021 or for any future

period. Certain information and footnote disclosures normally

included in financial statements prepared in accordance with GAAP

have been condensed or omitted. The accompanying unaudited

interim condensed consolidated financial statements should be read

in conjunction with the audited financial statements and notes

thereto for the year ended December 31, 2020, included in the

Company’s Annual Report on Form 10-K filed with the U.S.

Securities and Exchange Commission (the “SEC”) on March

25, 2021.

Functional

Currency

The Company's consolidated

functional currency is the U.S. Dollar. The Company's Australian

subsidiary and French subsidiary use the Australian Dollar and

European Euro, respectively, as their functional currency. At each

quarter-end, each foreign subsidiary's balance sheets are

translated into U.S. Dollars based upon the quarter-end exchange

rate, while their statements of operations and comprehensive loss

and statements of cash flows are translated into U.S. Dollars based

upon an average exchange rate during the period.

Comprehensive

Loss

Comprehensive loss represents net

loss plus any gains or losses not reported in the condensed

consolidated statements of operations and comprehensive loss, such

as foreign currency translations gains and losses that are

typically reflected on the Company’s condensed consolidated

statements of stockholders’ equity.

Use of

Estimates

The preparation of financial

statements in conformity with GAAP requires management to make

estimates and assumptions that affect the reported amounts of

assets and liabilities, disclosure of contingent assets and

liabilities, and reported amounts of expenses in the condensed

consolidated financial statements and accompanying notes. Actual

results could differ from those estimates.

Going

Concern Assessment

The Company applies Accounting

Standards Codification 205-40 (“ASC 205-40”),

Disclosure of Uncertainties about

an Entity’s Ability to Continue as a Going Concern,

which the Financial Accounting Standards Board (“FASB”)

issued to provide guidance on determining when and how reporting

companies must disclose going concern uncertainties in their

financial statements. ASC 205-40 requires management to perform

interim and annual assessments of an entity’s ability to

continue as a going concern within one year of the date of issuance

of the entity’s financial statements (or within one year

after the date on which the financial statements are available to

be issued, when applicable). Further, a company must provide

certain disclosures if there is “substantial doubt about the

entity’s ability to continue as a going concern.” In

April 2021, the Company analyzed its cash requirements through June

2022 and has determined that, based upon the Company’s

current available cash, the Company has no substantial doubt about

its ability to continue as a going concern.

MONOPAR

THERAPEUTICS INC.

NOTES TO

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31,

2021

Cash

Equivalents

The Company considers all highly

liquid investments purchased with a maturity of 90 days or less on

the date of purchase to be cash equivalents. Cash equivalents as of

March 31, 2021 and December 31, 2020 consisted of one money market

account.

Deferred

Offering Costs

Deferred offering costs represent

legal, auditing, travel and filing fees related to fundraising

efforts that have not yet been concluded.

Prepaid

Expenses

Prepayments are expenditures for

goods or services before the goods are used or the services are

received and are charged to operations as the benefits are

realized. Prepaid expenses may include payments to development

collaborators in excess of actual expenses incurred by the

collaborator, measured at the end of each reporting period.

Prepayments also include insurance premiums, dues and subscriptions

and software costs of $10,000 or more per year that are expensed

monthly over the life of the contract, which is typically one year.

Prepaid expenses are reflected on the Company’s condensed

consolidated balance sheets as other current assets.

Concentration

of Credit Risk

Financial instruments that

potentially subject the Company to concentration of credit risk

consist of cash and cash equivalents. The Company maintains cash

and cash equivalents at two reputable financial institutions. As of

March 31, 2021, the balance at one financial institution was in

excess of the $250,000 Federal Deposit Insurance Corporation

(“FDIC”) insurable limit. The Company has not

experienced any losses on its deposits since inception and

management believes the Company is not exposed to significant risks

with respect to these financial institutions.

Fair

Value of Financial Instruments

For financial instruments consisting

of cash and cash equivalents, accounts payable, accrued expenses,

and other current liabilities, the carrying amounts are reasonable

estimates of fair value due to their relatively short

maturities.

The Company adopted ASC 820,

Fair Value Measurements and

Disclosures, as amended, which addresses the measurement of

the fair value of financial assets and financial liabilities. Under

this standard, fair value is defined as the price that would be

received to sell an asset or paid to transfer a liability (i.e.,

the “exit price”) in an orderly transaction between

market participants at the measurement date.

The standard establishes a hierarchy

for inputs used in measuring fair value that maximizes the use of

observable inputs and minimizes the use of unobservable inputs by

requiring that the most observable inputs be used when available.

Observable inputs reflect assumptions market participants would use

in pricing an asset or liability based on market data obtained from

independent sources. Unobservable inputs reflect a reporting

entity’s pricing an asset or liability developed based on the

best information available under the circumstances. The fair value

hierarchy consists of the following three levels:

Level 1 - instrument valuations are

obtained from real-time quotes for transactions in active exchange

markets involving identical assets.

Level 2 - instrument valuations are

obtained from readily available pricing sources for comparable

instruments.

Level 3 - instrument valuations are

obtained without observable market values and require a high-level

of judgment to determine the fair value.

MONOPAR

THERAPEUTICS INC.

NOTES TO

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31,

2021

Determining which category an asset

or liability falls within the hierarchy requires significant

judgment. The Company evaluates its hierarchy disclosures each

reporting period. There were no transfers between Level 1, 2 or 3

of the fair value hierarchy during the three months ended March 31,

2021 and 2020. The following table presents the assets and

liabilities recorded that are reported at fair value on our

condensed consolidated balance sheets on a recurring basis. No

values were recorded in Level 2 or Level 3 at March 31, 2021 and

December 31, 2020.

Assets

and Liabilities Measured at Fair Value on a Recurring

Basis

|

March 31, 2021

|

|

|

|

|

Assets

|

|

|

|

|

Cash

equivalents(1)

|

|

$25,430,341

|

$25,430,341

|

|

Total

|

|

$25,430,341

|

$25,430,341

|

|

December 31,

2020

|

|

|

|

|

Assets

|

|

|

|

|

Cash

equivalents(1)

|

|

$16,605,682

|

$16,605,682

|

|

Total

|

|

$16,605,682

|

$16,605,682

|

(1)

Cash equivalents represent the fair value of the

Company’s investment in a money market account.

Net Loss

per Share

Net loss per share for the three

months ended March 31, 2021 and 2020 is calculated by dividing net

loss by the weighted-average shares of common stock outstanding

during the period. Diluted net loss per share for the three months

ended March 31, 2021 and 2020 is calculated by dividing net loss by

the weighted-average shares of the sum of a) weighted average

common stock outstanding (12,139,422 and 10,608,199 shares for the

three months ended March 31, 2021 and 2020, respectively) and b)

potentially dilutive shares of common stock (such as stock options

and restricted stock units) outstanding during the period. As of

March 31, 2021 and 2020, potentially dilutive securities included

stock-based awards to purchase up to 1,600,215 and 1,337,007 shares

of the Company’s common stock, respectively. For the three

months ended March 31, 2021 and 2020, potentially dilutive

securities are excluded from the computation of fully diluted net

loss per share as their effect is anti-dilutive.

Research

and Development Expenses

Research and development

(“R&D”) costs are expensed as incurred. Major

components of R&D expenses include salaries and benefits paid

to the Company’s R&D staff, fees paid to consultants and

to the entities that conduct certain R&D activities on the

Company’s behalf and materials and supplies which are used in

R&D activities during the reporting period.

MONOPAR

THERAPEUTICS INC.

NOTES TO

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31,

2021

Clinical

Trial Expense

The Company accrues and expenses the

costs for clinical trial activities performed by third parties

based upon estimates of the percentage of work completed over the

life of the individual study in accordance with agreements

established with contract research organizations, service

providers, and clinical trial sites. The Company determines the

estimates through discussions with internal clinical personnel and

external service providers as to progress or stage of completion of

trials or services and the agreed upon fee to be paid for such

services. Costs of setting up clinical trial sites for

participation in the trials are expensed immediately as R&D

expenses. Clinical trial site costs related to patient screening

and enrollment are accrued as patients are screened/entered into

the trial.

Collaborative

Agreements

The Company and its collaborative

partners are active participants in collaborative agreements and

all parties would be exposed to significant risks and rewards

depending on the technical and commercial success of the

activities. Contractual payments to the other parties in

collaboration agreements and costs incurred by the Company when the

Company is deemed to be the principal participant for a given

transaction are recognized on a gross basis in R&D expenses.

Royalties and license payments are recorded as earned.

During the three months ended March

31, 2021 and 2020, no milestones were met and no royalties were

earned, therefore, the Company did not pay or accrue/expense any

license or royalty payments.

Licensing

Agreements

The Company has various agreements

licensing technology utilized in the development of its product or

technology programs. The licenses contain success milestone

obligations and royalties on future sales. During the three months

ended March 31, 2021 and 2020, no milestones were met and no

royalties were earned, therefore, the Company did not pay or

accrue/expense any license or royalty payments under any of its

license agreements.

Patent

Costs

The Company expenses costs relating

to issued patents and patent applications, including costs relating

to legal, renewal and application fees, as a component of general

and administrative expenses in its condensed consolidated

statements of operations and comprehensive loss.

Income

Taxes

On December 16, 2015, the Company

began using an asset and liability approach for accounting for

deferred income taxes, which requires recognition of deferred

income tax assets and liabilities for the expected future tax

consequences of events that have been recognized in its financial

statements but have not been reflected in its taxable income.

Estimates and judgments are required in the calculation of certain

tax liabilities and in the determination of the recoverability of

certain deferred income tax assets, which arise from temporary

differences and carryforwards. Deferred income tax assets and

liabilities are measured using the currently enacted tax rates

that apply to taxable income in effect for the years in which those

tax assets and liabilities are expected to be realized or

settled.

MONOPAR

THERAPEUTICS INC.

NOTES TO

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31,

2021

The Company regularly assesses the

likelihood that its deferred income tax assets will be realized

from recoverable income taxes or recovered from future taxable

income. To the extent that the Company believes any amounts are not

“more likely than not” to be realized, the Company

records a valuation allowance to reduce the deferred income tax

assets. In the event the Company determines that all or part of the

net deferred tax assets are not realizable in the future, an

adjustment to the valuation allowance would be charged to earnings

in the period such determination is made. Similarly, if the Company

subsequently determines deferred income tax assets that were

previously determined to be unrealizable are now realizable, the

respective valuation allowance would be reversed, resulting in an

adjustment to earnings in the period such determination is

made.

Internal Revenue Code Sections 382

and 383 (“Sections 382 and 383”) limit the use of net

operating loss (“NOL”) carryforwards and R&D

credits, after an ownership change. To date, the Company has not

conducted a Section 382 or 383 study, however, because the Company

will continue to raise significant amounts of equity in the coming

years, the Company expects that Sections 382 and 383 will limit the

Company’s usage of NOLs and R&D credits in the

future.

ASC 740, Income Taxes, requires that the tax

benefit of net operating losses, temporary differences, and credit

carryforwards be recorded as an asset to the extent that management

assesses that realization is "more likely than not." Realization of

the future tax benefits is dependent on the Company's ability to

generate sufficient taxable income within the carryforward period.

The Company has reviewed the positive and negative evidence

relating to the realizability of the deferred tax assets and has

concluded that the deferred tax assets are not “more likely

than not” to be realized. As a result, the Company recorded a

full valuation allowance as of March 31, 2021 and December 31,

2020. U.S. Federal R&D tax credits from 2016 to 2019 were

utilized to reduce payroll taxes in future periods and were

recorded as other current assets for amounts anticipated to be

received within 12 months and other non-current assets for amounts

anticipated to be received beyond 12 months on the Company’s

condensed consolidated balance sheets. The Company intends to

maintain the valuation allowance until sufficient evidence exists

to support its reversal. The Company regularly reviews its tax

positions. For a tax benefit to be recognized, the related tax

position must be “more likely than not” to be sustained

upon examination. Any amount recognized is generally the largest

benefit that is “more likely than not” to be realized

upon settlement. The Company’s policy is to recognize

interest and penalties related to income tax matters as an income

tax expense. For the three months ended March 31, 2021 and 2020,

the Company did not have any interest or penalties associated with

unrecognized tax benefits.

The Company is subject to U.S.

Federal, Illinois and California income taxes. In addition, the

Company is subject to local tax laws of France and Australia. Tax

regulations within each jurisdiction are subject to the

interpretation of the related tax laws and regulations and require

significant judgment to apply. The Company was incorporated on

December 16, 2015 and is subject to U.S. Federal, state and local

tax examinations by tax authorities for the tax years 2015 through

2020. The Company does not anticipate significant changes to its

current uncertain tax positions through March 31, 2021. The Company

plans on filing its U.S. Federal and state tax returns for the year

ended December 31, 2020 prior to the extended filing deadlines in

all jurisdictions.

Stock-Based

Compensation

The Company accounts for stock-based

compensation arrangements with employees, non-employee directors

and consultants using a fair value method, which requires the

recognition of compensation expense for costs related to all

stock-based awards, including stock option and restricted stock

unit (“RSU”) grants. The fair value method requires the

Company to estimate the fair value of stock-based payment awards on

the date of grant using an option pricing model or the closing

stock price on the date of grant in the case of RSUs.

MONOPAR

THERAPEUTICS INC.

NOTES TO

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31,

2021

Stock-based compensation expense for

awards granted to employees, non-employee directors and consultants

are based on the fair value of the underlying instrument calculated

using the Black-Scholes option-pricing model on the date of grant

for stock options and using the closing stock price on the date of

grant for RSUs and recognized as expense on a straight-line basis

over the requisite service period, which is the vesting period.

Determining the appropriate fair value model and related

assumptions requires judgment, including estimating the future

stock price volatility, forfeiture rates and expected terms. The

expected volatility rates are estimated based on the actual

volatility of comparable public companies over recent historical

periods of the same length as the expected term. The Company

selected these companies based on reasonably comparable

characteristics, including market capitalization, stage of

corporate development and with historical share price information

sufficient to meet the expected term (life) of the stock-based

awards. The expected term for options granted to date is estimated

using the simplified method. Forfeitures are estimated at the time

of grant and revised, if necessary, in subsequent periods if actual

forfeitures differ from those estimates. The Company has not paid

dividends and does not anticipate paying a cash dividend in the

future vesting period and, accordingly, uses an expected dividend

yield of zero. The risk-free interest rate is based on the rate of

U.S. Treasury securities with maturities consistent with the

estimated expected term of the awards.

Note 3 - Capital

Stock

Holders of the common stock are

entitled to receive such dividends as may be declared by the Board

of Directors out of funds legally available therefor. Upon

dissolution and liquidation of the Company, holders of the common

stock are entitled to a ratable share of the net assets of the

Company remaining after payments to creditors of the Company. The

holders of shares of common stock are entitled to one vote per

share for the election of each director nominated to the Board and

one vote per share on all other matters submitted to a vote of

stockholders.

The Company’s amended and

restated certificate of incorporation authorizes the Company to

issue 40,000,000 shares of common stock with a par value of $0.001

per share.

Sales of Common Stock

On January 13, 2020, the Company

entered into a Capital on Demand™ Sales Agreement with

JonesTrading, as sales agent, pursuant to which Monopar may offer

and sell (at its discretion), from time to time, through or to

JonesTrading shares of Monopar’s common stock, having an

aggregate offering price of up to $19.7 million. Pursuant to this

agreement, during the three months ended March 31, 2020, the

Company sold 33,903 shares of its common stock at an average gross

price per share of $16.00 for net proceeds of $508,043 after fees,

commissions and offering costs of $34,384. Also pursuant to this

agreement, during the three months ended March 31, 2021, the

Company sold 1,104,047 shares of its common stock at an average

gross price per share of $10.20 for net proceeds of $10,925,311

after fees and commissions of $338,153. In aggregate pursuant to

this agreement, the Company sold 1,964,724 shares of its common

stock at an average gross price per share of $10.02 for net

proceeds of $19,100,602, after fees and commissions of

$591,188.

As of March 31, 2021, the Company

had 12,569,933 shares of common stock issued and

outstanding.

Note 4 - Stock

Incentive Plan

In April 2016, the Company’s

Board of Directors and stockholders representing a majority of the

Company’s outstanding stock at that time, approved the

Monopar Therapeutics Inc. 2016 Stock Incentive Plan, as amended

(the “Plan”), allowing the Company to grant up to an

aggregate 700,000 shares of stock-based awards in the form of stock

options, restricted stock units, stock appreciation rights and

other stock-based awards to employees, non-employee directors and

consultants. In October 2017, the Company’s Board of

Directors voted to increase the stock award pool to 1,600,000

shares of common stock, which subsequently was approved by the

Company’s stockholders. In April 2020, the Company’s

Board of Directors voted to increase the stock award pool to

3,100,000 (and increase of 1,500,000 shares of common stock), which

was approved by the Company’s stockholders in June

2020.

MONOPAR

THERAPEUTICS INC.

NOTES TO

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31,

2021

During the three months ended March

31, 2021, the Company’s Plan Administrator Committee (with

regards to non-officer employees and consultants) and the

Company’s Compensation Committee, as ratified by the Board of

Directors (in the case of executive officers and non-employee

directors) granted to executive officers, non-officer employees,

consultants and non-employee directors aggregate stock options for

the purchase of 196,476 shares of the Company’s common stock

with exercise prices ranging from $5.76 to $9.67 which vest from

one year to four years. All stock option grants have a 10-year

term. In addition, an aggregate 124,374 restricted stock units were

granted to executive officers, non-officer employees and

non-employee directors which vest over one to four

years.

Under the Plan, the per share

exercise price for the shares to be issued upon exercise of an

option shall be determined by the Plan Administrator, except that

the per share exercise price shall be no less than 100% of the fair

market value per share on the grant date. Fair market value is the

Company’s closing price on Nasdaq. Stock options generally

expire after 10 years.

Stock option activity under the Plan

was as follows:

|

|

|

|

|

Number of

Shares Subject to Options

|

Weighted-Average Exercise

Price

|

|

Balances at January 1,

2020

|

1,087,463

|

$

2.94

|

|

Granted

|

174,357

|

14.08

|

|

Forfeited

|

(3,243)

|

8.47

|

|

Balances at December 31,

2020

|

1,258,577

|

4.47

|

|

Granted(1)

|

196,476

|

6.93

|

|

Forfeited(2)

|

(3,344)

|

17.25

|

|

Exercised

|

(2,913)

|

6.00

|

|

Balances at March 31,

2021

|

1,448,796

|

4.77

|

(1)

196,476 options vest as follows: options to

purchase 168,704 shares of the Company’s common stock vest

6/48ths on the six-month anniversary of grant date and 1/48th per

month thereafter; options to purchase 17,772 shares of the

Company’s common stock vest quarterly over one year; and

options to purchase 10,000 shares of the Company’s common

stock vest monthly over one year. Exercise prices range from $5.76

to $9.67 per share.

(2)

Forfeited

options represent unvested shares and vested, expired shares

related to employee terminations.

A summary of

options outstanding as of March 31, 2021 is shown

below:

|

Exercise

Prices

|

|

Number of Shares

Subject to Options Outstanding

|

|

Weighted-Average

Remaining Contractual Term in Years

|

|

Number of Shares

Subject to Options Fully Vested and Exercisable

|

|

Weighted-Average

Remaining Contractual Term in Years

|

|

$0.001-$5.00

|

|

557,420

|

|

5.47

|

|

555,670

|

|

5.46

|

|

$5.01-$10.00

|

|

732,519

|

|

7.98

|

|

400,390

|

|

7.28

|

|

$10.01-$15.00

|

|

146,732

|

|

8.84

|

|

74,428

|

|

8.84

|

|

$15.01-$20.00

|

|

12,125

|

|

8.09

|

|

8,583

|

|

7.81

|

|

|

|

1,448,796

|

|

|

|

1,039,071

|

|

|

MONOPAR

THERAPEUTICS INC.

NOTES TO

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31,

2021

Restricted stock unit activity under

the Plan was as follows:

|

|

|

Weighted-Average Grant Date

Fair Value per Unit

|

|

Unvested balance at January

1, 2020

|

—

|

$

—

|

|

Granted

|

45,722

|

12.93

|

|

Vested

|

(5,156)

|

12.93

|

|

Forfeited

|

(500)

|

12.93

|

|

Unvested balance at January

1, 2021

|

40,066

|

12.93

|

|

Granted

|

124,374

|

6.81

|

|

Vested

|

(13,021)

|

11.52

|

|

Unvested Balance at March 31,

2021

|

151,419

|

8.02

|

During the three months ended March

31, 2021 and 2020, the Company recognized $246,343 and $220,765 of

employee and non-employee director stock-based compensation expense

as general and administrative expenses, respectively, and $111,589

and $100,171 as research and development expenses, respectively.

The stock-based compensation expense is allocated on a departmental

basis, based on the classification of the stock-based award holder.

No income tax benefits have been recognized in the condensed

consolidated statements of operations and comprehensive loss for

stock-based compensation arrangements.

The Company recognizes as an expense

the fair value of options granted to persons (currently

consultants) who are neither employees nor non-employee directors.

Stock-based compensation expense for consultants which were

recorded as research and development expense for the three months

ended March 31, 2021 and 2020 was $10,300 and $17,561,

respectively.

The fair value of options granted

from inception to March 31, 2021 was based on the Black-Scholes

option-pricing model assuming the following factors: 4.7 to 6.2

years expected term, 55% to 85% volatility, 0.4% to 2.9% risk free

interest rate and zero dividends. The expected term for options

granted to date was estimated using the simplified method. There

were 196,476 and 163,357 stock options granted during the three

months ended March 31, 2021 and 2020, respectively. For the three

months ended March 31, 2021 and 2020, the weighted-average grant

date fair value was $4.90 and $9.34 per share, respectively. For

the three months ended March 31, 2021 and 2020 the fair value of

shares vested was $0.3 million and $0.2 million, respectively. At

March 31, 2021, the aggregate intrinsic value of outstanding stock

options was approximately $3.6 million of which approximately $3.5

million was vested and approximately $0.1 million is expected to

vest (representing options to purchase 409,725 shares of the

Company’s common stock expected to vest), and the

weighted-average exercise price in aggregate was $4.77 which

includes $3.49 for fully vested stock options and $8.01 for stock

options expected to vest. At March 31, 2021, unamortized unvested

balance of stock-based compensation was $3.2 million, to be

amortized over 3.0 years.

MONOPAR

THERAPEUTICS INC.

NOTES TO

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31,

2021

Note 5 - Related

Party Transactions

As of March 31, 2021, Tactic Pharma,

LLC (“Tactic Pharma”), the Company’s initial

investor, beneficially owned 34.0% of Monopar’s common stock

and during the three months ended March 31, 2021, there were no

transactions between Tactic Pharma and Monopar.

None of the related parties

discussed below received compensation other than market-rate

salary, market-rate stock-based compensation and benefits and

performance-based bonus or in the case of non-employee directors,

market-rate Board fees and market-rate stock-based compensation.

The Company considers the following individuals as related parties:

Three of the Company’s board members were also Managing

Members of Tactic Pharma as of March 31, 2021. Chandler D. Robinson

is the Company’s Co-Founder, Chief Executive Officer, common

stockholder, Managing Member of Tactic Pharma, former Manager of

the predecessor LLC, Manager of CDR Pharma, LLC and Board member of

Monopar as a C Corporation. Andrew P. Mazar is the Company’s

Co-Founder, Executive Vice President of Research and Development,

Chief Scientific Officer, common stockholder, Managing Member of

Tactic Pharma, former Manager of the predecessor LLC and Board

member of Monopar as a C Corporation. Michael Brown is a Managing

Member of Tactic Pharma (as of February 1, 2019 with no voting

power as it relates to Monopar), a previous managing member of

Monopar as an LLC, common stockholder and Board member of Monopar

as a C Corporation.

Note 6 –

Commitments and Contingencies

License,

Development and Collaboration Agreements

Onxeo

S.A.

In June 2016, the Company executed

an option and license agreement with Onxeo S.A.

(“Onxeo”), a public French company, which gave Monopar

the exclusive option to license (on a world-wide exclusive basis)

Validive to pursue treating severe oral mucositis in patients

undergoing chemoradiation treatment for head and neck cancers. The

pre-negotiated Onxeo license agreement for Validive as part of the

option agreement includes clinical, regulatory, developmental and

sales milestones that could reach up to $108 million if the Company

achieves all milestones, and escalating royalties on net sales from

5% to 10%. On September 8, 2017, the Company exercised the license

option, and therefore paid Onxeo the $1 million fee under the

option and license agreement.

Under the agreement, the Company is

required to pay royalties to Onxeo on a product-by-product and

country-by-country basis until the later of (1) the date when a

given product is no longer within the scope of a patent claim in

the country of sale or manufacture, (2) the expiry of any extended

exclusivity period in the relevant country (such as orphan drug

exclusivity, pediatric exclusivity, new chemical entity

exclusivity, or other exclusivity granted beyond the expiry of the

relevant patent), or (3) a specific time period after the first

commercial sale of the product in such country. In most countries,

including the U.S., the patent term is generally 20 years from the

earliest claimed filing date of a non-provisional patent

application in the applicable country, not taking into

consideration any potential patent term adjustment that may be

filed in the future or any regulatory extensions that may be

obtained. The royalty termination provision pursuant to (3)

described above is shorter than 20 years and is the least likely

cause of termination of royalty payments.

MONOPAR

THERAPEUTICS INC.

NOTES TO

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31,

2021

The Onxeo license agreement does not

have a pre-determined term, but expires on a product-by-product and

country-by-country basis; that is, the agreement expires with

respect to a given product in a given country whenever the

Company’s royalty payment obligations with respect to such

product have expired. The agreement may also be terminated early

for cause if either the Company or Onxeo materially breach the

agreement, or if either the Company or Onxeo become insolvent. The

Company may also choose to terminate the agreement, either in its

entirety or as to a certain product and a certain country, by

providing Onxeo with advance notice.

The Company is internally developing

Validive and has activated clinical sites and began dosing for its

VOICE clinical trial, which, if successful, may allow the Company

to apply for marketing approval within the next several years. The

Company will need to raise significant funds or enter into a

collaboration partnership to support the further development,

including potential commercialization of Validive. As of March 31,

2021, the Company had not reached any of the pre-specified

milestones and has not been required to pay Onxeo any funds under

this license agreement other than the $1 million one-time license

fee.

Grupo

Español de Investigación en Sarcomas

(“GEIS”)

In

June 2019, the Company executed a clinical collaboration agreement

with GEIS for the development of camsirubicin in patients with

advanced soft tissue sarcoma (“ASTS”). Following

completion of the dose escalation run-in clinical trial in the U.S.

(or another country) that Monopar currently anticipates initiating

in the second half of 2021, the Company continues to expect that

GEIS will sponsor and lead a multi-country, randomized, open-label

Phase 2 clinical trial to evaluate camsirubicin head-to-head

against the current first-line treatment for ASTS, doxorubicin. The

Company will provide study drug and supplemental financial support

for the clinical trial averaging approximately $2 million to $3

million per year. During the three months ended March 31, 2021, the

Company incurred $0.3 million in expenses under the GEIS agreement

and other clinical-related expenses including clinical material

manufacturing and database management expenses in support of

GEIS’s Phase 2 camsirubicin clinical trial. During the three

months ended March 31, 2020, the Company provided a nominal amount

of financial support and incurred a nominal amount of drug

manufacturing costs under the GEIS agreement. The Company can

terminate the agreement by providing GEIS with advance notice, and

without affecting the Company’s rights and ownership to any

intellectual property or clinical data.

XOMA

Ltd.

The intellectual property rights

contributed by Tactic Pharma to the Company included the

non-exclusive license agreement with XOMA Ltd. for the humanization

technology used in the development of MNPR-101. Pursuant to such

license agreement, the Company is obligated to pay XOMA Ltd.

clinical, regulatory and sales milestones for MNPR-101 that could

reach up to $14.925 million if the Company achieves all milestones.

The agreement does not require the payment of sales royalties.

There can be no assurance that the Company will reach any

milestones under the XOMA agreement. As of March 31, 2021, the

Company had not reached any milestones and has not been required to

pay XOMA Ltd. any funds under this license agreement.

MONOPAR

THERAPEUTICS INC.

NOTES TO

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

March 31,

2021

Operating

Leases

The Company is currently leasing

office space for its executive headquarters at 1000 Skokie Blvd.,

in the Village of Wilmette, Illinois for $4,487 per month on a

month-to-month basis.

During the three months ended March

31, 2021 and 2020, the Company recognized operating lease expenses

of $13,462 and $13,483, respectively.

Legal

Contingencies

The Company may be subject to claims

and assessments from time to time in the ordinary course of

business. No claims have been asserted to date.

Indemnification

In the normal course of business,

the Company enters into contracts and agreements that contain a

variety of representations and warranties and provide for general

indemnification. The Company’s exposure under these

agreements is unknown because it involves claims that may be made

against the Company in the future, but that have not yet been made.

To date, the Company has not paid any claims nor been required to

defend any action related to its indemnification obligations.

However, the Company may record charges in the future as a result

of future claims against these indemnification

obligations.

In accordance with its second

amended and restated certificate of incorporation, amended and

restated bylaws and the indemnification agreements entered into

with each officer and non-employee director, the Company has

indemnification obligations to its officers and non-employee

directors for certain events or occurrences, subject to certain

limits, while they are serving at the Company’s request in

such capacities. There have been no claims to date.

Item 2.

Management's Discussion and

Analysis of Financial Condition and Results of

Operations.

You should read the following

discussion and analysis of our financial condition and results of

operations together with our condensed consolidated financial

statements and related notes contained in this Quarterly Report on

Form 10-Q. Some of the information contained in this discussion and

analysis or set forth elsewhere in this Quarterly Report on Form

10-Q, including information with respect to our plans and strategy

for our business and related financing activities, includes

forward-looking statements that involve risks and

uncertainties.

Overview

We are a clinical stage biopharmaceutical

company primarily focused on developing proprietary therapeutics

designed to extend life or improve quality of life for cancer

patients. We are building a drug development pipeline through the

licensing and acquisition of therapeutics in late preclinical and

clinical development stages. We leverage our scientific and

clinical experience to help reduce the risk of and accelerate the

clinical development of our drug product candidates.

Under our Capital on DemandTM Sales Agreement

with JonesTrading Institutional Services, LLC

(“JonesTrading”), through March 31, 2021, we have sold

1,964,724 shares of our common stock at an average gross price of

$10.02 per share for net proceeds of $19,100,602, after fees and

commissions of $591,188.

In February

2021, we announced the first patient dosed in our Phase 2b/3 VOICE

trial of Validive® for the

prevention of CRT-induced severe

oral

mucositis in patients with

oropharyngeal cancer

(“VOICE”).

Given the COVID-19 pandemic and its effects on clinical trials, we

have adjusted our clinical development plans accordingly to fit

what is feasible in the current environment. We have simplified the

design of the previously planned Phase 3 clinical trial for our

lead product candidate, Validive, to a seamless, adaptive Phase

2b/3 clinical trial design (our VOICE trial) that will allow us to

minimize touch points with patients and sites. This trial design

will allow us to immediately advance to the Phase 3 portion of the

trial if supported by the interim data at the end of the Phase 2b

portion of the trial. To complete the VOICE clinical program,

including, if required, completing a smaller second Phase 3

confirmatory clinical trial, we will require additional funding in

the millions or tens of millions of dollars (depending on if we

have consummated a collaboration or partnership or neither for

Validive), which we are planning to pursue within the next 12

months.

In June 2019, we

executed a clinical collaboration agreement with Grupo Español

de Investigación en Sarcomas (“GEIS”) for the

development of camsirubicin in patients with advanced soft tissue

sarcoma (“ASTS”). Based on our current inability to

gain regulatory approval to initiate the camsirubicin Phase 2

clinical trial in Spain, we are evaluating alternatives to move the

dose escalation run-in clinical trial forward outside of Spain. We

believe that we will be able to initiate the run-in clinical trial

in the second half of 2021 in the U.S. or another country.

Following completion of the run-in clinical trial, we continue to

expect that GEIS will sponsor and lead a multi-country, randomized,

open-label Phase 2 clinical trial to evaluate camsirubicin

head-to-head against the current first-line treatment for ASTS,

doxorubicin. We believe we have funds sufficient to obtain topline

results from the dose escalation “run-in” clinical

trial. Additional funding will be required to support further

development beyond the run-in clinical trial.

Pursuant to our 50/50 collaboration development agreement with

NorthStar Medical Radioisotopes, LLC (“NorthStar”) to

develop potential Radio-Immuno-Therapeutics (“RITs”) to

treat severe COVID-19 (patients with SARS-CoV-2 infection), we have

coupled MNPR-101 to therapeutic radioisotopes supplied by

NorthStar. The resulting conjugates are designed to be highly

selective agents that have the potential to kill aberrantly

activated cytokine-producing immune cells. By eradicating these

cells with a uPAR-targeted RIT (“uPRIT”), the goal is

to spare healthy cells while quickly reducing the cytokine storm

and its harmful systemic effects. Through April 30, 2021, we have

incurred immaterial expense related to the NorthStar collaboration,

while partnering with several key companies and institutions to

further the collaboration’s development efforts. These

collaborators include: IsoTherapeutics Group, LLC, which generated

the uPRIT candidates; Aragen Bioscience Inc., which screened the

uPRIT candidates through preclinical biochemical testing; and Texas

Lung Injury Institute / University of Texas Health Science Center

at Tyler, which plans to perform preclinical testing and, if

successful, clinical testing.

In